from:China Electricity Councildate:2014-03-19

CEC publishes the Demand/Supply Analysis and Forecast of China Power Industry 2014

Electric power operation was safe and stable; and power demand and supply was overall balanced in 2013. Total power consumption increased by 7.5% compared to the previous year, a 1.9 percentage point up. Power consumption in tertiary industry and in household kept a high increase rate at 10.3% and 9.2% respectively. Secondary industry power consumption increased by 7.0% compared to the previous year; and growth rate of consumption in manufacturing rose by quarter while consumption of the four most energy intensive industry rose 6.0% with growth rate going down and then up. All regions experienced higher growth rate in consumption than the previous year; and Western China region kept the lead among all areas. Total generating capacity by the end of 2013 in China reached 1.25TWh, leaping to the first in the world for the first time. In all newly-installed capacity, non-fossil accounted for 62%; hydropower reached record high; and integrated solar power rocketed to ten times that of the previous year. Wind power maintained rapid growth: utilization rose another 151 hours compared with the previous year and availability of equipment improved significantly.

For 2014, China’s economy will maintain steady development with an expected GDP growth rate of about 7.5%. Correspondingly, growth rate of total power consumption is expected to be 7.0%; and total power capacity is expected to reach 1.34TW by the end of 2014. Power supply and demand will be overall balanced: supply in Northeastern region is expected to experience a large surplus while surplus in Northwestern region is also expected; in Northern region, supply is a little short but basically balanced with demand; in other regions (Eastern, Central and Southern China regions), supply and demand will be overall balanced.

I. Power Demand and Supply Analysis 2013

1. Growth rate of total power consumption increased compared with the previous year

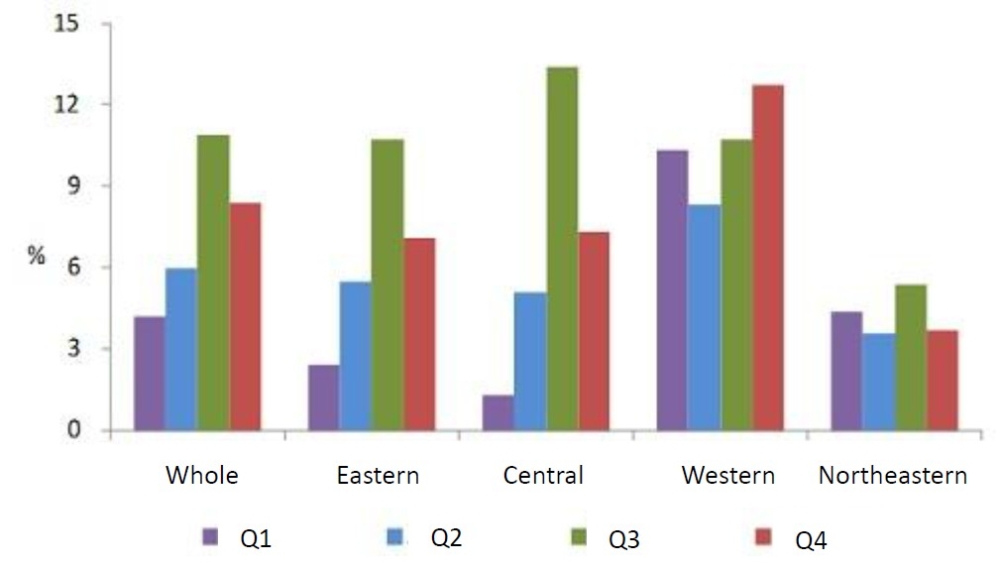

According to CEC statistics, total power consumption in 2013 was 5320TWh, a 7.5% increase from the previous year, 1.9 percentage points higher than the 2013 growth rate, and power consumption per capita will reach 3911KWh. Under the influence of steady economic rebound, continuous high temperature in summer and relatively warm weather in winter, the first three quarters experienced consecutive increase in power consumption growth, reaching a highest 10.9% in the third quarter, and that of the fourth quarter dropped a little but still reached 8.4%, surpassing that of the previous year.

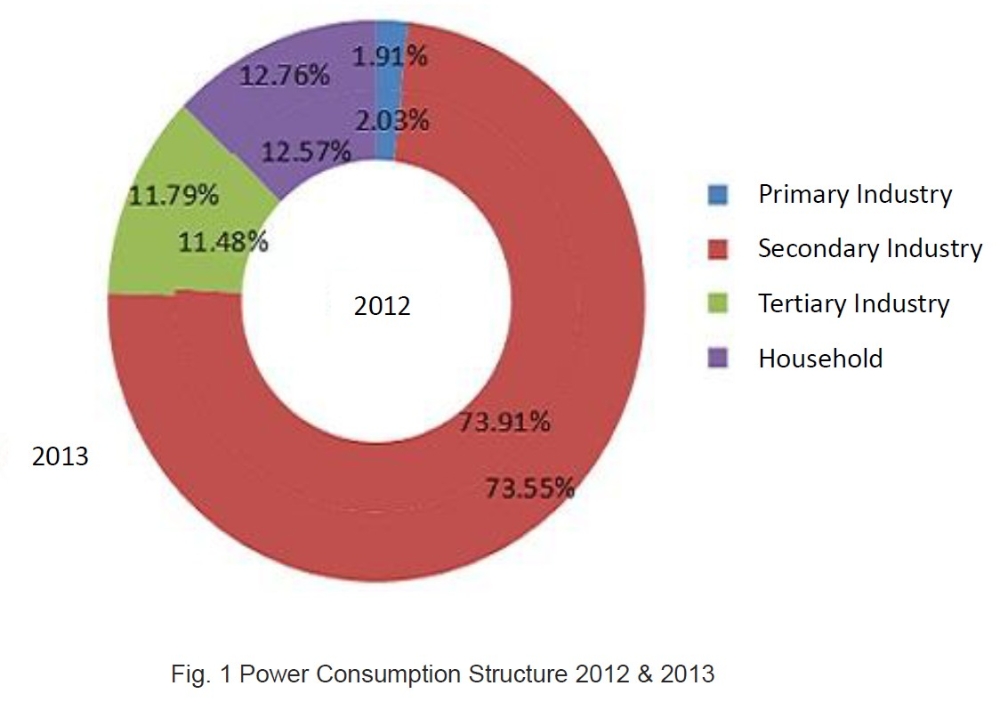

Tertiary industry and household power consumption maintained high speed growth. Tertiary industry consumption increased by 10.3%, reflecting the continuous activeness of tertiary market demand, and its ratio to total power consumption increased by 0.3 percentage point. Household power consumption increased by 9.2%, ratio to total power consumption increased by 0.19 percentage point. The continuous high temperature in most of China in the third quarter gave a 17.6% rise to household power consumption compared to previous year.

Consumption growth in manufacturing industry increased each quarter while consumption growth rate of the four most energy intensive industry went down and then up. Power consumption of secondary industry was increased by 7.0%, 2.8 percentage points higher than that of the previous year; contribution to total power consumption was increased to 68.7%, 13.6 percentage points higher than that of the previous year. Power consumption in manufacturing was increased by 6.8%, with quarterly growth rate of 4.5%, 5.0%, 8.0% and 9.3% respectively, reflecting the steady growth of real economy production. Consumption of chemical, construction material, ferrous metal and nonferrous metal industry together had a growth rate of 6.0%, quarterly rate are 5.3%, 3.3%, 6.9% and 8.6% respectively, experiencing a 0.43 percentage point decrease from the previous year.

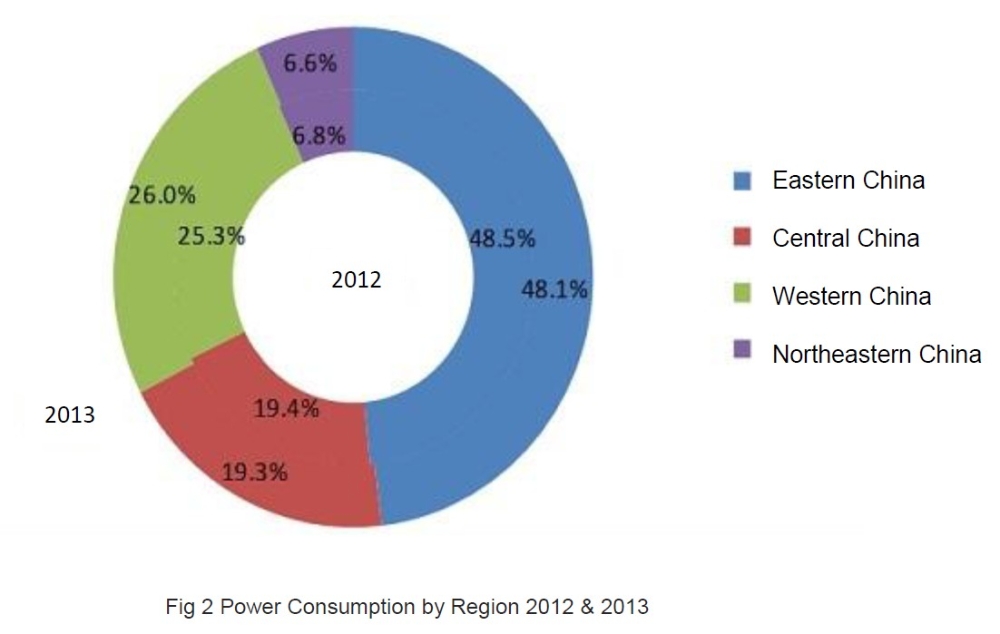

Western China continued leading the growth in power consumption, while other regions’ growth rates also surpass those of the previous year. Growth rate of power consumption reached 6.6%, 6.9%, 10.6% and 4.2% respectively. The proportion of Western China power consumption in total consumption went up by 0.7 percentage point than the previous year.

2. Total installed capacity ascended to the first in the world; New energy generating capacity kept super speed growth

Investment in grid accounted for 51.2% of total power engineering investment, 1.6 percentage points up from the previous year. Among investment in power generation, non-fossil fuel accounted for 75.1%, 1.7 percentage points increase from the previous year. Newly installed non-fossil fuel generation capacity reached 58.29GW, increasing its proportion in total newly installed capacity to 62%. By the end of 2013, total installed capacity of China reached 1.25TW, surpassing the United States and becoming the largest in the world for the first time. 390GW, or 31.6% of the capacity came from non-fossil fuel. Total power generation was increased by 7.5% to 5350TWh. Utilization hours of generation facility was 4511 hours, 68 down from the previous year. Standard coal consumption of thermal power plants remained world class and reached 321g/KWh, realizing the Energy saving and Emissions reduction target of the national Twelfth Five-Year Plan ahead of schedule.

Hydropower capacity newly operated reached record high. Capacity of conventional hydropower reached 260GW with 28.73GW newly installed, with a growth rate of 12.9%. Newly installed capacity of pumped storage was 1200MW, adding its total capacity by the end of 2013 to 21.51GW.

Newly installed capacity of integrated solar power rose almost by tenfold. In 2013, a series of policy was published to support the development of solar power industry by the State Council and various relevant Ministries, incentivizing solar power industry. Newly installed capacity was increased by 953.2% to 11.3GW while total capacity by the end of 2013 was increased by 335.1% to 14.79GW. Total generation was increased by 143.0% to 8.7TWh.

Wind power remained high speed growth and utilization hours had a clear rise. Newly installed capacity reached 14.06GW, making the total capacity 75.48GW by the end of 2013, 24.5% more than the previous year. Generation was increased by 36.3% to 140.1TWh; utilization experienced growth for two consecutive years, reaching the highest since year 2008 to 2080 hours, 151 hours higher than the previous year.

Investment in nuclear power decreased; a total of two nuclear units went into operation in 2013. Investment was 22.4% lower than the previous year. Newly installed capacity was 2.21GW and total capacity reached 14.61GW, 16.2% higher than the previous year. Generation went up by 14.0%; while utilization went up 38 hours to 7893 hours.

Investment in and proportion of capacity of coal-fired power kept going down while gas-fired capacity grew rapidly. Investment in coal-fired power was decreased by 12.3%, and its proportion in total generation investment went down to 19.6%. Installed capacity of coal-fired power was 790GW by 2013, accounting for 63.0% of total installed capacity, 2.6 percentage points down from the previous year. Generation went up by 6.7% while its proportion went down 0.6 percentage point to 73.8%. Utilization was 5128 hours. By the end of 2013, gas-fired power installed capacity and generation increased by 15.9% and 4.7% respectively.

Inter-region power transmission kept high-speed growth. Total inter-regional power transmission reached 237.9TWh, 17.9% higher than the previous year; inter-provincial power transmission was 785.3TWh, up by 9.1%. Sichuan province transmitted 54.7TWh power to Eastern China, 185.8% more than the previous year, through Xiangshang DC and Jinsu DC transmission lines in order to expend surplus hydropower. West-East Transmission within the range of China Southern Grid increased by 5.8% to 131.4TWh.

Coal supply was adequate while natural gas supply was tight. Domestic coal market had ample supply; coal price went down and then up in 2013. Natural gas demand soared; supply tightened in winter, restraining some gas-fired power generation capacity. Since the government rose the of non-residential natural gas in July 2013, some gas-fired generation companies had been experiencing continuous deficit.

3. Power demand and supply were balanced overall; while surplus and inadequacy existed in different regions

In 2013, power demand and supply in China was basically balanced. Supply exceeded demand in Northeastern and Northwestern China; Northern, Central and Southern China experienced overall balance; and Eastern China had a tight supply where peak shifting and averting occurred in Jiangsu province and Zhejiang province

II. Power Supply and Demand Forecast 2014

1. Growth rate of power consumption is expected to fall slightly

National economy will keep its steady development with an expected 7.5% GDP growth rate. Considering the overall economic situation, the national effort to deal with air pollution, energy saving and emissions reduction, resolving the severe over capacity of energy intensive industries, and the relatively large base of consumption because of the continuous high temperature in summer 2013, total power consumption is expected to increase by 6.5% to 7.5%, 7.0% being the recommended rate.

2. Power generating capacity suffices; proportion of non-fossil fuel capacity keeps increasing

Newly installed capacity is expected to be around 96GW, among which 60GW is non-fossil fuel capacity, 30GW is coal-fired capacity. Total generating capacity is expected to reach 1.34TW, among which 820GW comes from coal-fired generation, 450GW from non-fossil fuel, accounting for 34% of total generating capacity. Among non-fossil fuel, capacity of conventional hydropower is 280GW, pumped storage 22.71GW, nuclear 21.09GW, integrated wind 93GW, integrated solar 29GW.

3. Overall balance of power supply and demand in 2014

National power supply and demand is expected to be balanced overall in 2014. There will be large surplus in generating capacity in Northeastern China and certain surplus in the Northwest; capacity in Northern China will be balanced with a little tightness; and Eastern, Central and Southern will also experience overall balance. Utilization is expected to reach 4430 to 4480 hours, among which coal-fired facility utilization exceeds 5100 hours.

III. Suggestions

1. Speed up clean energy generation

To coordinate the planning of clean energy generation strategically; to improve relevant rules, regulations and technical standards; to implement policies and take measures to promote distributed power generation; to improve financing mechanism and tax incentives; to promote green power trade; and to encourage clean energy technological innovation to lower cost.

2. Formulate and carry out “Substitution with Electric Power” planning

To publish “Substitution with Electric Power” planning and policy; to carry out “Substitution with Electric Power” projects in major fields as industry, transportation, construction, agriculture and residential life; to adjust power structure; to promote energy saving and emissions reduction through market; and to improve operation, maintenance and management of environmental protection equipment in power enterprises.

3. Solve the wind curtailment problem in Northern, Northeastern and Northwestern China

To persist the policy of centralized and distributed coordination while put a focus on distributed wind in recent years; to strengthen overall planning and improve development mechanism; to enhance management and implementation.

4. Address the capacity surplus in Northeastern China

To carry out research on this specific topic and to propose plans and measures to deal with the problem; to strictly control the amount of newly installed capacity in the region.

5. Rationalize power and heat price mechanism

To promote two-part power pricing system (capacity price & KWh charges); to formulate independent transmission and distribution pricing mechanism; to publish guidance on regional heat price and to approve different prices in regions with large deficit in heat supply.

6. Perfect the special limit on air pollutant emissions

To propose a technical guideline and more scientific regulations to meet the limit; to adjust power prices in regions with special limit; to coordinate outage renovation; and to finance environmental protection technological innovation projects in key regions.

Tel:+86-25-84152563

Fax:+86-25-52146294

Email:export@hbtianrui.com

Address:Head Office: No.8 Chuangye Avenue, Economic Development Zone, Tianmen City, Hubei Province, China (Zip Code: 431700) Nanjing Office: Room 201-301, Building K10,15 Wanshou Road,Nanjing Area, China (Jiangsu) Pilot Free Trade Zone,Jiangsu Province,China (Zip Code:211899)